You are shopping for a semi in East York, your broker sends you a rate hold offer, and the Bank of Canada decision is only two weeks away. Do you lock in now or wait to see what happens on July 15? That is the question a lot of Toronto buyers and homeowners coming up for renewal are working through right now.

The Bank of Canada is Canada’s central bank. It sets the overnight rate, which is the interest rate banks charge each other for short-term loans. That rate influences what you pay on a variable mortgage and what lenders use as a starting point for fixed rates. On June 10, 2026, the Bank held that key rate at 2.25 percent. The next announcement lands July 15, along with a full Monetary Policy Report (MPR) that lays out the Bank’s read on inflation and growth.

Nobody knows the July 15 outcome yet, and I will not guess at it here. Below I explain what the June hold means for Toronto mortgages right now, and what to check before you make a financing decision in the next few weeks.

Why the June Rate Hold Still Matters

Think of it this way. The Bank of Canada left its target for the overnight rate at 2.25 percent on June 10, 2026. The Bank Rate, which is what the Bank charges on short-term loans to financial institutions, sits at 2.5 percent. The rate paid on deposit notes is 2.20 percent.

Those numbers set the floor for the lending stack that Toronto banks and monoline lenders use to price your mortgage. A hold does not mean nothing is moving underneath it. Bond markets shift every day, and fixed mortgage rates track those bond yields more closely than they track the overnight rate.

June sales data from the Toronto Regional Real Estate Board (TRREB) showed buyers coming back into the market even with listings staying tight. You can read more about that in my breakdown of Toronto and GTA home sales in June 2026. Rate stability did not make the city cheap. It just removed one source of surprise for buyers who had already qualified under the current stress test.

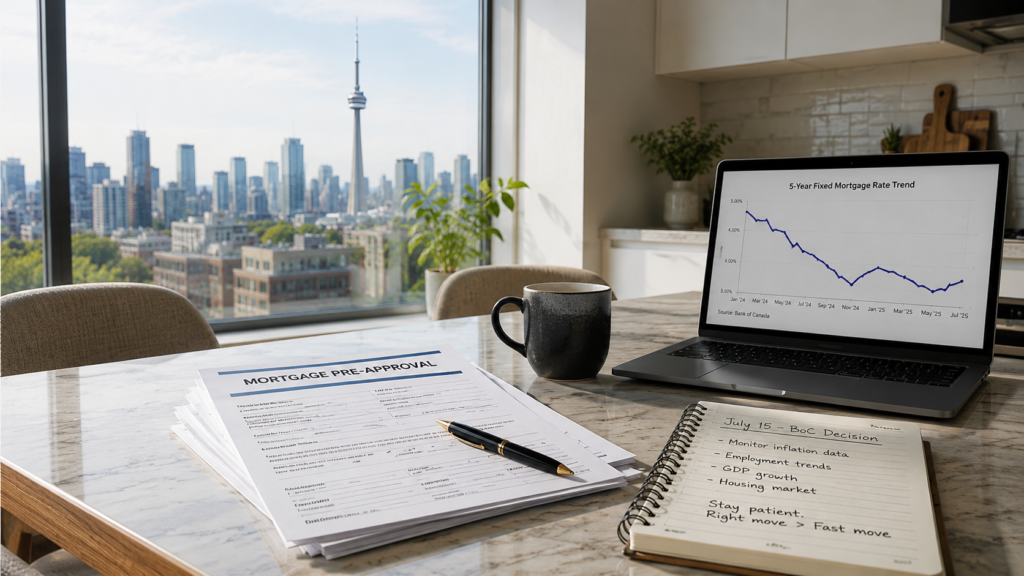

Toronto Mortgage Outlook Before July 15

Here is the honest picture heading into the July 15 announcement. Well qualified borrowers have been seeing five-year fixed offers in the low four percent range through late June 2026, though your actual quote depends on your down payment, your amortization, and whether your mortgage is insured.

Fixed rates move with Government of Canada bond yields, not with the Bank of Canada headline. If yields drift down before July 15, some lenders will cut their fixed offers without waiting for a policy announcement. If yields rise on inflation data or global news, fixed rates can climb even if the Bank holds again on July 15.

Variable rates work differently. They are tied to prime, and prime only moves when the Bank’s policy rate moves. The June hold kept prime steady. The July 15 statement and the accompanying report will tell markets whether the Bank sees more room to cut, or whether it is done for now.

Fixed vs Variable Right Now

When I work with buyers choosing between fixed and variable this month, I tell them to look at the spread between the two rather than trying to predict the next Bank of Canada meeting. When that spread is small, locking into a fixed rate removes the uncertainty of July 15 entirely.

If you already qualify comfortably and have room in your budget, a variable rate still gives you the benefit of any future cuts without the cost of breaking a fixed term early. There is no universally correct answer here. It depends on your risk tolerance and how tight your monthly budget already is.

Two rules matter more than the rate itself right now. First, check the insured mortgage cap if you are putting down less than 20 percent, because it directly affects your maximum purchase price. Second, confirm whether a 30-year amortization applies to your purchase, since that changes your monthly payment more than a small rate move ever will.

Questions to Ask Before You Lock

Before you commit to a fixed rate or decide to float through July 15, work through this list with your mortgage broker or lender.

- When does your pre-approval expire, and will your lender refresh it without a full re-application

- What is the gap between your quoted contract rate and the minimum qualifying rate used in the federal stress test

- Do you qualify for insured financing, and how does that change your maximum purchase price

- Does a 30-year amortization apply to your situation, or are you limited to 25 years

- How wide is the spread between the fixed and variable offers you have received

- Can you get a 90 or 120 day rate hold that carries you past July 15 without forcing a decision today

- If your mortgage renews within the next year, will you switch lenders or stay put

- Are you buying a condo or a freehold property, since lenders and insurers treat them differently at the same rate

None of these questions require guessing what happens on July 15. They just require paying attention to numbers that are already known.

What July 15 Means for Your Toronto Mortgage Outlook

Renewals are the quiet part of every mortgage conversation. Purchase headlines get the attention, but thousands of GTA households renew their mortgage every month, and the rules are not the same for everyone.

If you renew with your existing lender through a straight switch, you may qualify at your contract renewal rate instead of the federal stress test rate.

Since November 2024, the Office of the Superintendent of Financial Institutions (OSFI) has also exempted straight-switch renewals to a new federally regulated lender from the prescribed minimum qualifying rate, as long as the loan amount and amortization do not increase and you are not taking new money out. The new lender still underwrites your file, but you are not automatically tested at contract rate plus two per cent the way a brand-new purchase would be.

If you refinance, extend your amortization, or borrow additional funds at renewal, the stress test rules for a new purchase generally apply again. That is a different conversation from a simple renewal, and worth sorting out with your broker before you assume you can shop freely.

If you are up for renewal in the next 12 months, start shopping 120 days out rather than 30. Closings and paperwork do not wait for a favourable headline from the Bank of Canada.

Final Thoughts

The Bank of Canada held at 2.25 percent on June 10, 2026, and the next decision arrives July 15 with a full Monetary Policy Report. I am not going to pretend I know that outcome before it happens, and you should be wary of anyone who claims they do.

What you can control right now is your own preparation. Watch bond yields and lender spreads rather than only the overnight rate. Run your stress test math before you fall for a listing. Use a rate hold if you need time to get through the announcement without a rushed decision.

Once July 15 passes, the picture will get clearer. Until then, plan around what is already confirmed rather than what might be coming.